Date: Apr 10, 2018

Battery materials and electric vehicles offer something unique to today’s commodity producers and investors: a sustainable growth story that is not just China-dependent. The exponential growth in demand is creating a scramble for resources not seen since the last great commodity super cycle.

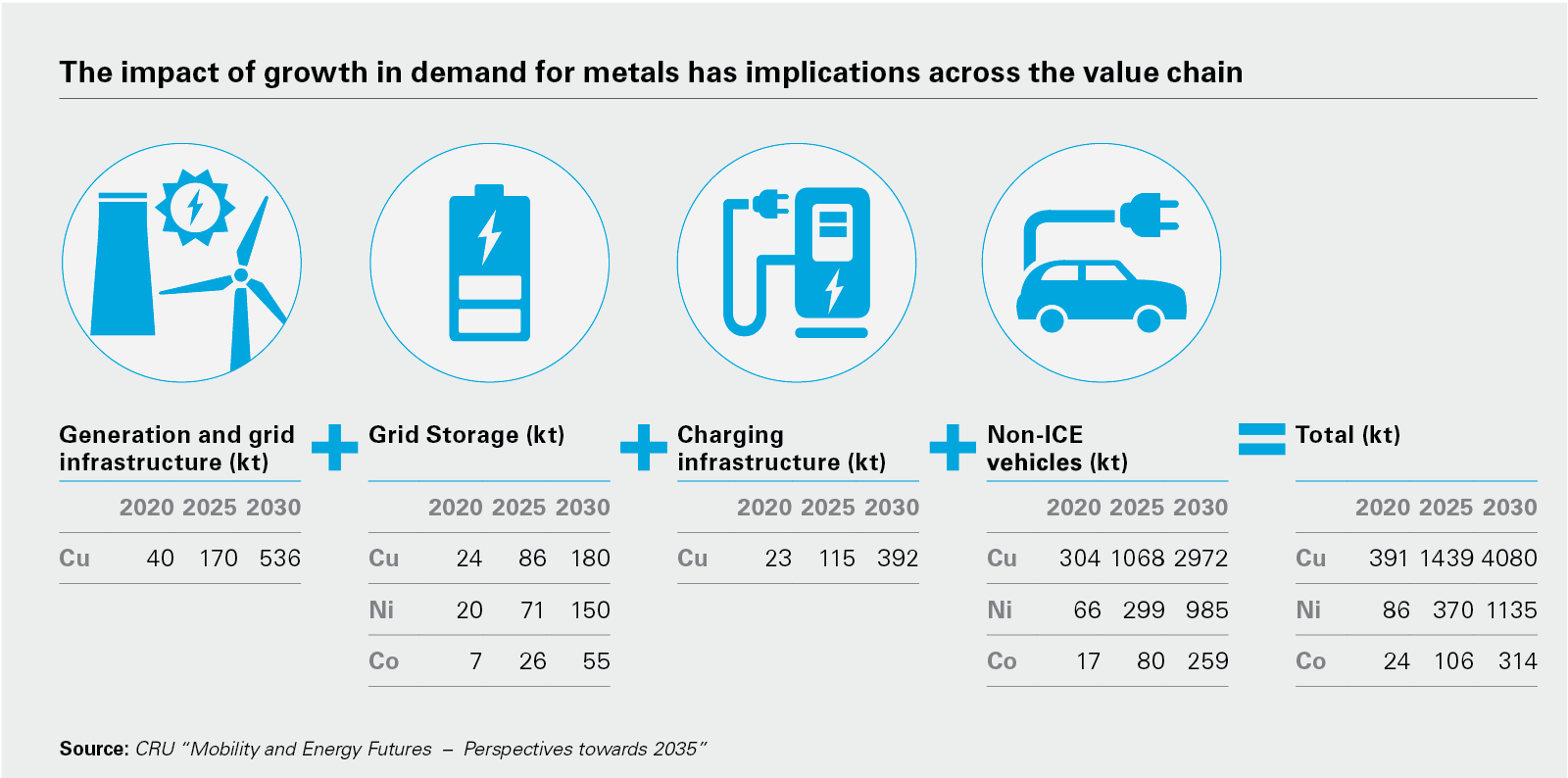

Effective battery capacity must expand by more than 12 times today’s levels to meet the expected demand for electric vehicles (EVs) and renewable energy storage by 2025, when the global battery market is projected to be worth US$100 billion, according to World Economic Forum.

With EVs forecast to make up more than half of car sales within two decades, the electrification revolution is going to be built around six key commodities: copper, nickel, lithium, cobalt, manganese and graphite. Copper and nickel are already key industrial metals, traded on global exchanges with consumers experienced in managing supply risk. Manganese and graphite supply give no cause for concern at the moment, which leaves cobalt and lithium.

Securing supply

Cobalt, mined as a by-product with 60 per cent of supply coming from the Congo, will be the most challenging material on the supply front. Prices have tripled since the start of 2016 in anticipation of future demand. Apple, Samsung and BMW are among companies that have already sought to tie down long-term supply arrangements, but have met significant resistance from miners reluctant to agree to deals at a time of sharply rising prices. Lithium prices have surged in the last three years amid a shortage of the material, and deficits are expected to continue in the short term. However, there are dozens of new projects in development, and the existing dominant suppliers have latent capacity they can bring online.

But the big challenge—especially for car makers—will be securing high quality product that can be refined into battery-grade material. Major automakers are already beginning to make their move. Ford has announced it will invest US$11 billion by 2022 in electrification, and expand its suite to 40 EVs globally including 16 full battery vehicles by the same year. Toyota has started making investments too, taking a 15 per cent stake in Australian-listed lithium producer Orocobre. Competition for supply from the low cost, high quality producers will increase, while miners whose product is not in demand will fall by the wayside.